Spring is just around the corner, and if you're like many folks, you might be dreaming about cruising in a shiny new car. Dealerships love to tempt us with those flashy 0% financing offers to get us through the door. It sounds too good to be true, right? Well, maybe it is. Let's dive in and crunch the numbers to see what's really going on.

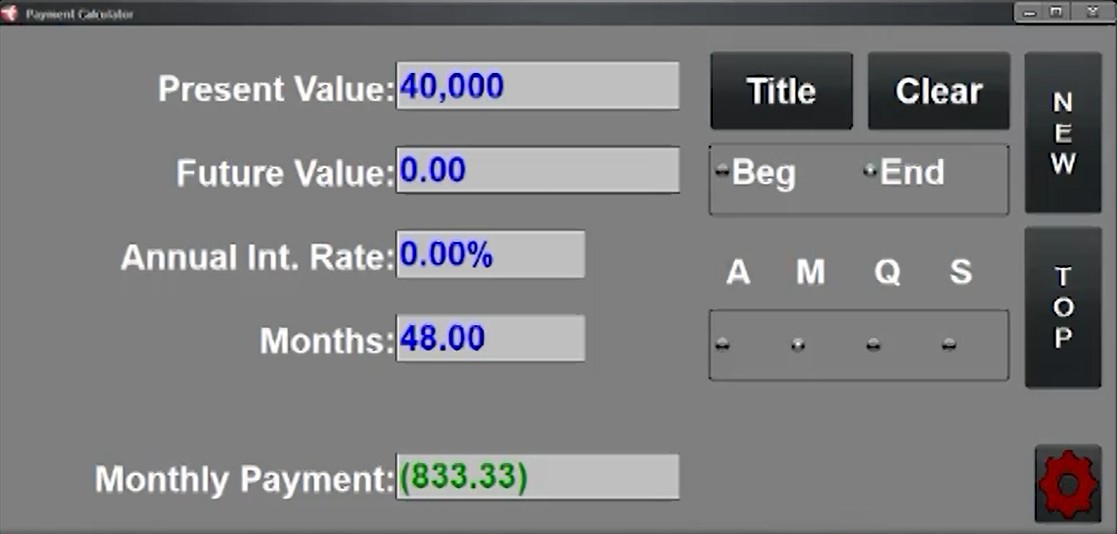

The Setup: A $40,000 Car Dream

Imagine you've got your eye on a new car priced at $40,000. For simplicity, we're skipping taxes, title, and licensing fees here—just focusing on the base price to make the math crystal clear.

Dealerships often push a 0% interest deal over 48 months (that's 4 years). On the surface, this seems straightforward: no interest means you're just dividing the cost evenly. But is there more to it? Let's compare it to an alternative where you take a cash rebate and finance through a bank or credit union.

Option 1: The 0% Financing Deal

With 0% interest, your monthly payment is simply the total cost divided by the number of months. Here's the math:

- Loan amount (principal, P): $40,000

- Interest rate (annual): 0%

- Loan term (n): 48 months

Since there's no interest, the formula simplifies to:

Monthly Payment (PMT) = P / n PMT = $40,000 / 48 = $833.33

So, you'd pay $833.33 each month for 48 months, totaling $40,000 exactly. No extra costs, right? Hold that thought.

Here is the “easy” math:

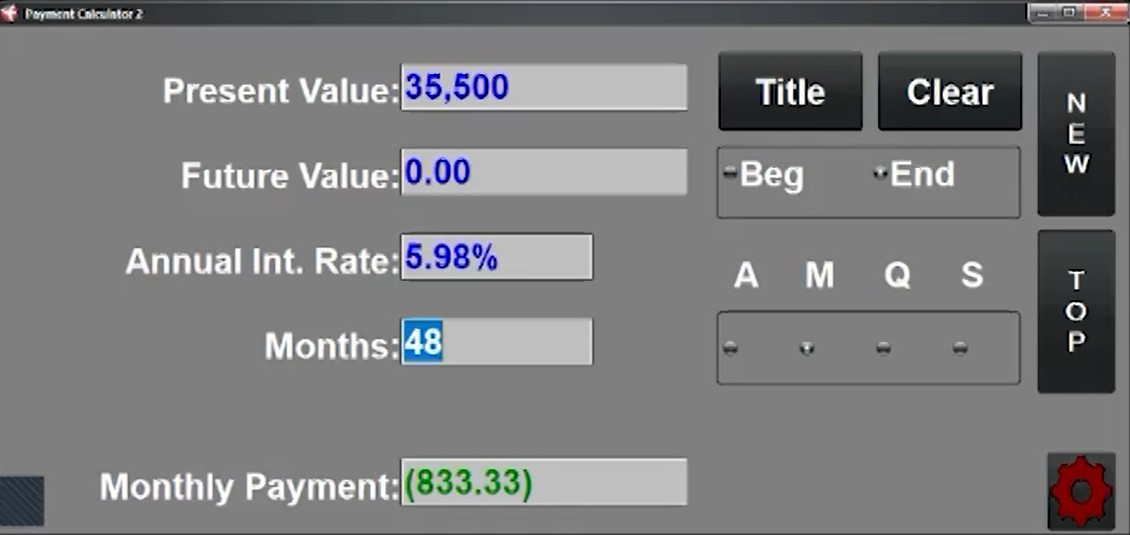

Option 2: Cash Rebate + Bank Loan

Now, let's say the dealership offers a $4,500 rebate to clear the lot (this happens often!). Instead of taking the 0% deal, you apply the rebate, dropping the price to $35,500, and get a loan from your local bank or credit union at around 6% interest. For precision, we'll use 5.976%—a rate that might be available depending on your credit.

- Original price: $40,000

- Rebate: -$4,500

- Loan amount (P): $35,500

- Interest rate (annual): 5.976%

- Monthly interest rate (r): 5.976% / 12 / 100 = 0.00498 (or 0.498%)

- Loan term (n): 48 months

For “detailed” folks – Here’s the “college” version of the math:

To calculate the monthly payment, we use the standard loan amortization formula:

PMT = P × [r × (1 + r)^n] / [(1 + r)^n - 1]

Plugging in the numbers:

First, calculate (1 + r)^n = (1.00498)^48 ≈ 1.2672 (you can use a calculator or spreadsheet for this)

Then, numerator: r × (1 + r)^n ≈ 0.00498 × 1.2672 ≈ 0.00631

Denominator: (1 + r)^n - 1 ≈ 1.2672 - 1 = 0.2672

So, PMT ≈ $35,500 × (0.00631 / 0.2672) ≈ $35,500 × 0.02351 ≈ $833.33

Surprise! The monthly payment is still $833.33—the exact same as the 0% deal.

Here is the “easy” math:

The Big Reveal: Where's the Hidden Interest?

How is this possible? The $4,500 rebate exactly offsets the interest you'd pay on the lower loan amount. In other words:

- In the 0% deal, the dealer builds the cost of financing (about $4,500 in implied interest) right into the $40,000 price tag.

- With the rebate, you're buying the car for its "true" price without that baked-in interest, then paying actual interest to the bank—but it nets out the same monthly.

The rebate deal is simply the price of the car without the cost of the loan interest, and the zero-interest financing deal really hides the interest cost within the car price so you don't easily see it.

Over 48 months, the total paid in both scenarios is the same: 48 × $833.33 = $40,000. But in the rebate option, you're effectively getting a discount upfront and paying interest separately, while the 0% hides it.

Why This Matters: Think Like a Wealth Creator

When you understand the real cost behind flashy financing offers and how your cash flow can serve you better elsewhere, you start thinking like a wealth creator, not a consumer. Don't let zero-percent hype blind you—always compare rebates and outside financing.

The Financialoscopy team wants to empower you to see the truth more clearly. But the real power is when you align your decisions with truth, integrity, and long-term prosperity. If you would like our team to run some numbers for your own scenario, reach out. We'll fire up our calculators. It's time to schedule your Financialoscopy!